By : [Abhishek Tiwari]

In the ever-shifting landscape of global finance, a new chapter is unfoldingâone that raises more than a few eyebrows. Central Bank Digital Currencies (CBDCs) emerge not just as protagonists but as potential agents of financial upheaval, casting shadows on the traditional understanding of money and triggering concerns about privacy, surveillance, and governmental interference.

Picture a world where financial transactions leave an indelible trace in the digital realm, a world ushered in by CBDCsâinnovations that promise a revolution but also signal a potential financial dystopia.

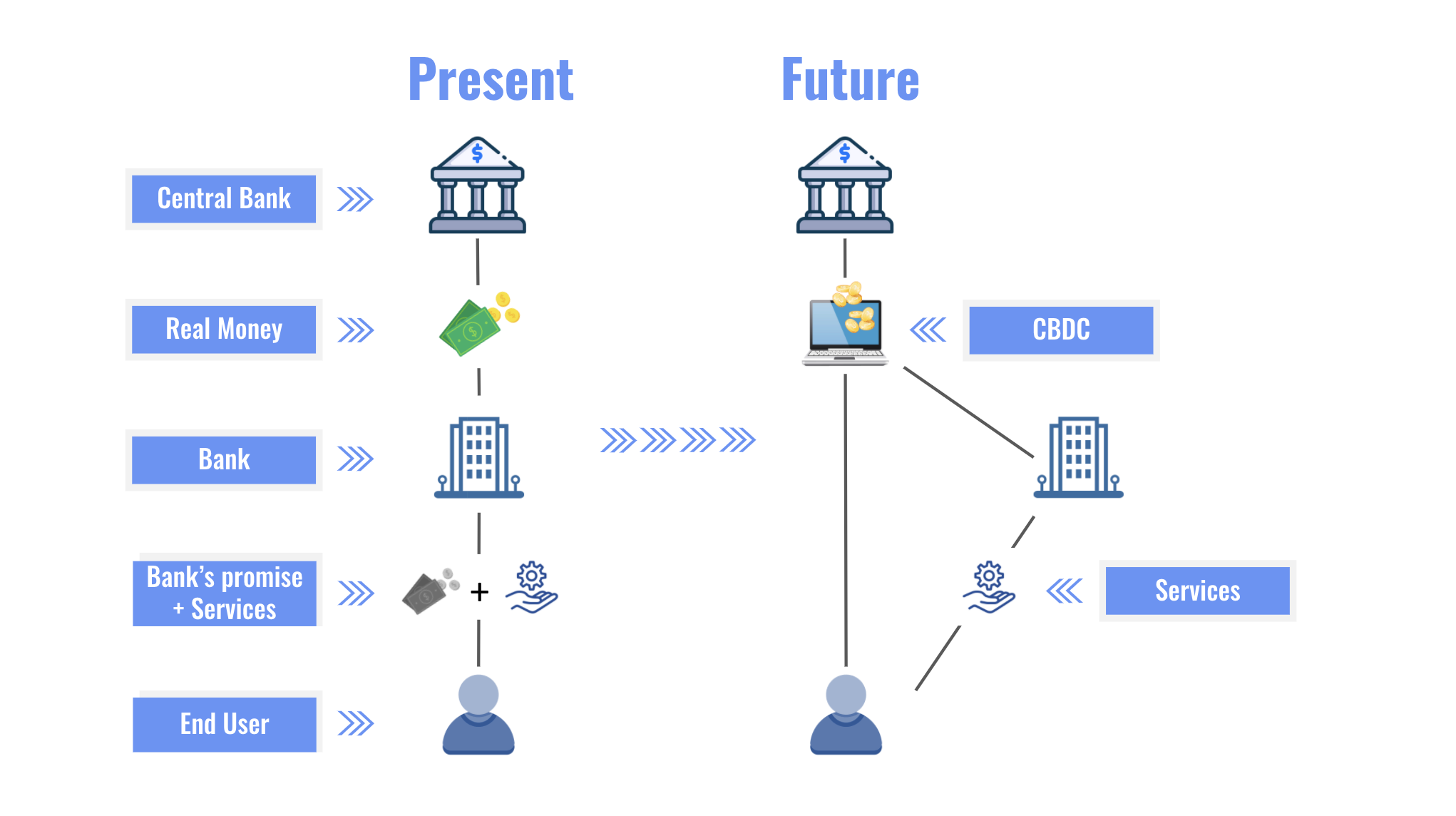

At the heart of this digital metamorphosis lies the concept of CBDCs, a concept that, while intriguing, raises red flags. Imagine your nation's currency transformed into the binary code of the digital realm, where the central bank takes center stage in an unprecedented symphony of financial control. No longer confined to the physicality of bills and coins, CBDCs become dynamic forces, shaping a future marred by concerns of governmental overreach.

But this journey is not without its skeptics. As CBDCs strive to break barriers, the question arises: Are they inclusive havens or trojan horses that compromise financial privacy? The promise of inclusivity becomes a double-edged sword as the shadows of traceable transactions loom large, leaving individuals exposed in the digital spotlight.

As we traverse this digital terrain, some CBDCs showcase not just intelligence but a potential Pandora's box. They can execute contracts, automate financial transactions, and dance to the tune of programmable money. The question arises: Is this a beacon of progress or a dangerous leap into uncharted financial territory?

Yet, as with any grand voyage, challenges abound, and the shadows cast by CBDCs become more pronounced. The transparency of transactions threatens the very essence of privacy. As transactions become traceable, a new era of financial surveillance emerges, leaving individuals vulnerable to unwarranted scrutiny.

In the realm of cybersecurity, an unsung hero becomes a reluctant protagonist. The vulnerability of CBDCs to cyber threats becomes a subplot in our narrative. As we embark on this digital odyssey, the stakes are high, and the guardianship of personal data becomes paramount.

And what of traditional banking structures? The stability we've known for decades faces potential disruptions, and the foundations of traditional banks tremble in the wake of CBDCs. As Central Banks become direct competitors to payment service providers, banks might lose income. Likewise, a new form of investment opportunity may reduce consumer deposit demand. In return, this could reduce bank lending to overall economy and hence, economic growth. It's a delicate dance between innovation and the fear of financial instability, where the outcome remains uncertain.

The HRFâs just-launched Central Bank Digital Currency Tracker profiles each country taking steps toward a CBDC, and links these moves on a web page with information on that countryâs record on human rights and corruption. In compiling the tracker, HRF found that âdictatorships are leading the charge in CBDC deployment.â HRF estimates that 3.7 billion people â 46% of the world population â live under dictatorships experimenting with CBDCs.

CBDCs are vulnerable to electricity outages and insufficient internet connectivity

Implementing CBDCs becomes our hero's quest, a journey fraught with technical, regulatory, and logistical challenges. The call to create a digital currency is not just an innovation but a potential invitation for government interference and manipulation within the financial system.

China: Digital Currency Electronic Payment (DCEP)

In the dystopian streets of China, the Digital Currency Electronic Payment (DCEP) unfolds not as a marvel, but as a harbinger of societal control with its own set of ominous financial shadows. Everyday transactions pulse with life, courtesy of programmable money and the allure of offline capabilities.

Features: DCEP goes beyond being a digital surrogate, designed to seamlessly facilitate everyday transactions. However, the shadows of increased surveillance raise concerns about privacy. The delicate balance between technological progress and individual rights becomes a cause for scrutiny, foreshadowing a future where personal freedoms are sacrificed.

Past Record: China's history of financial opacity and government interference in banking is a dark backdrop to the unfolding narrative. The DCEP's potential to extend the government's reach into personal financial transactions adds a layer of concern, given the country's track record of suppressing dissent and infringing on individual liberties.

United States: Digital Dollar Project

In the vast, despondent landscapes of the United States, the Digital Dollar Project emerges not as a beacon of progress but as a testament to efficiency and inclusivity, albeit with its share of uncertainties. A private-sector initiative, it aims to reshape the financial landscape in a narrative tinged with shades of corporate control.

Features: Efficiency and inclusivity take center stage in this narrative, but the shadows of regulatory challenges and data security loom large, casting doubt on the project's potential impact on individual liberties. Ongoing legislative discussions mark the narrative, but the outcome remains uncertain in a story clouded by ambiguity.

Past Record: The U.S. has a complex history of financial regulation, with frequent debates on privacy and government intervention. The Digital Dollar Project's success depends on clear boundaries defined by a well-defined regulatory framework, an aspiration that seems increasingly elusive in a world dominated by corporate interests.

Sweden: E-Krona

![]()

As we traverse the desolate landscapes of Sweden, the E-Krona unfolds as a narrative of adaptability, but not without its financial pitfalls. It's a digital evolution focused on maintaining access to currency in a cashless society, portraying a society devoid of the familiar comforts of physical cash.

Features: E-Krona's spotlight is on accessibility, aspiring to be a resilient alternative to physical cash in a world where anonymity is scarce. However, challenges arise, especially in rural areas, and privacy concerns persist, casting a gloom over the potential erosion of personal freedoms.

Past Record: Sweden's past record of financial innovation is overshadowed by the potential challenges of integrating a digital currency into existing structures. The balancing act between progress and protection becomes increasingly precarious in a narrative steeped in shadows.

European Union: Eurozone CBDC

![]()

Our journey concludes in the mosaic of nations forming the European Union, where the Eurozone CBDC seeks not to complement physical cash, but to forge a path of control and conformity in a bleak financial landscape.

Features: The Eurozone CBDC narrative revolves around complementing physical cash, enhancing cross-border payments, and fostering financial innovationâideals that mask a darker intent of centralized control. Regulatory harmonization becomes a focal point, ensuring a consistent and safe user experience, but at the cost of individual financial autonomy.

Past Record: The diverse regulatory landscapes among EU member states pose challenges for seamless integration, painting a picture of a fragmented financial dystopia. Navigating these challenges becomes crucial for a secure and consistent user experience, though the shadow of centralized control looms large.

Safe Aspects: The safety of the Eurozone CBDC lies in successfully navigating regulatory challenges. If it achieves harmonization among EU member states, it can contribute to a secure and consistent user experience in the digital financial landscape

As our critical exploration of the digital odyssey unfolds, a parallel narrative emergesâthe human side of the digital saga. Privacy, once a sacred right, becomes a character in our story, facing erosion in the face of traceable transactions and the fear of unwarranted surveillance.

Government surveillance, once a distant concept, becomes a potential antagonist. The misuse of CBDC technology could grant unprecedented access to citizens' financial transactions, a narrative reminiscent of Orwellian nightmares threatening the right to financial privacy.

Financial inclusion, once a beacon of hope, faces the shadows of potential discrimination. The misuse of CBDCs could lead to selective access, violating principles of equal treatment and inclusivity. It's a subplot that challenges the very essence of financial freedom.

For those venturing into the uncharted territory of CBDCs, resources become your compass.

These resources offer a glimpse into the evolving landscape, providing insights, research, and updates on the digital odyssey.

As we sail through the uncharted waters tainted by past financial flaws and government interference, our narrative takes unexpected turns. From the bustling streets of China to the serene landscapes of Sweden, the legislative battlegrounds of the United States, and the coordinated efforts of the European Union, the digital odyssey is a tapestry woven with innovation, challenges, and human narratives.

Privacy, cybersecurity, and financial stability become characters in our dystopian story, each playing a crucial role in shaping the narrative of CBDCs amidst the haunting specters of past financial flaws and potential government interference. It's not just a journey of digital evolution; it's a quest for balance, where progress meets protection, and the shadows of past financial flaws and government intrusion loom large.

In this dystopian odyssey, let's stay informed, ask probing questions, and navigate with wisdom. As we explore the uncharted waters of CBDCs tainted by past financial flaws and potential government interference, let our rights, privacy, and financial landscape remain secure and resilient. The future is digitalâlet's embark on this journey with open minds, wise hearts, and a critical eye on the shadows of past financial flaws and governmental interference that may threaten our financial freedom.